What Happens To Your Housing Loan Once You Sell Your House?

TLDR When selling your home in Singapore, ensure you pay off your outstanding home loan, refund any CPF monies used,...

Read More

TLDR

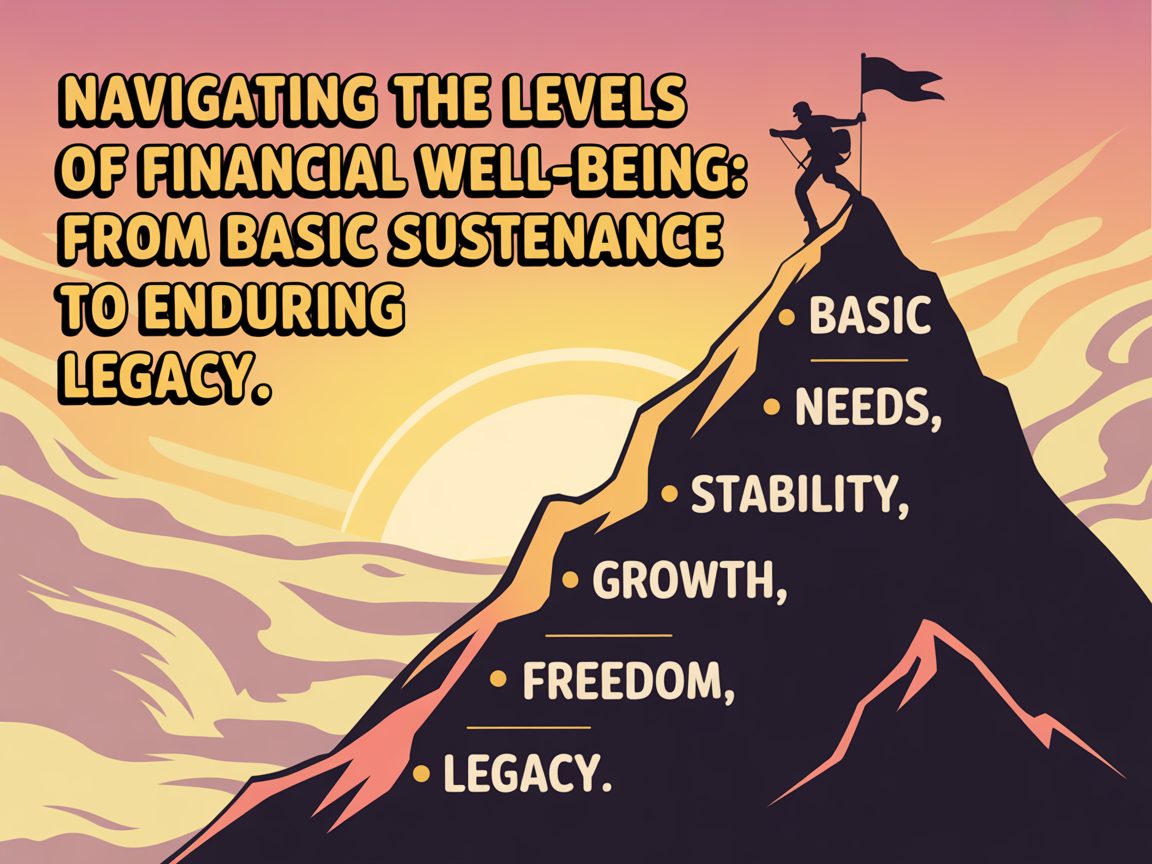

The journey to financial wealth involves progressing through seven stages, from Survival to Legacy, each with distinct goals and challenges. Starting with managing essentials and debts in Survival, building savings in Stability, and creating an emergency fund in Security, the path continues through Growth by investing and increasing assets. Financial Independence is reached when passive income covers living expenses, granting freedom from traditional work. Abundance allows generous living and purposeful investments, while Legacy focuses on long-term impact through estate planning and philanthropy. Progression is non-linear and requires disciplined budgeting, saving, and learning. Real estate decisions like buying or selling depend on individual circumstances and expert advice can provide clarity. Mastering these stages with consistent habits and strategic planning leads to lasting financial well-being and the ability to support future generations.

When the concept of “wealth” comes to mind, many envision opulent vehicles, sprawling estates, or exotic vacations. Yet, the journey to financial prosperity isn’t a single destination; rather, it’s a dynamic progression through distinct phases of accumulation and stewardship.

Various frameworks exist to describe these stages of financial development. One such notable model, popularized by financial expert Ramit Sethi, outlines seven levels of wealth, spanning from mere survival to comprehensive legacy planning. Each level presents its unique set of challenges and objectives. Understanding your current position within this spectrum can empower you to more effectively address hurdles and advance your financial journey.

Below, we explore these levels of financial well-being, detailing their characteristics and offering strategies to progress from simply surviving to building a lasting legacy.

1. Survival: The Foundation

At the foundational “Survival” stage, your income barely meets your essential living costs. You might find yourself caught in a cycle of living paycheck to paycheck, struggling with numerous bills, or burdened by high-interest debt that merely keeps you afloat.

The primary objective here is to gain a clear understanding of your financial landscape, including your earnings and obligations, and to halt any uncontrolled outflow of funds. This involves establishing a simple budget, identifying and cutting unnecessary expenditures, and actively seeking avenues to boost your income.

If you are at this level, practical tools such as debt consolidation, community support networks, or professional career coaching can provide much-needed relief. For instance, in Singapore, individuals grappling with substantial unsecured, high-interest debt might consider the Debt Management Programme (DMP). Non-profit organizations like Credit Counselling Singapore (CCS) facilitate this program, aiding in the structured repayment of debts with major banks and credit card providers.

2. Stability: Building a Buffer

Advancing to the “Stability” phase signifies a capacity to consistently meet your financial obligations and begin systematically reducing debt. While the immediate pressure of financial panic subsides, a degree of vulnerability remains. Unexpected events like job loss or significant medical expenses could easily revert you to survival mode.

To solidify this stage, implementing a disciplined approach to financial management is crucial. Automating bill payments and savings can help ensure consistency and build a crucial financial buffer.

3. Security: Establishing Your Safety Net

The “Security” stage is characterized by consistent financial command. Your expenses are comfortably covered, debts are manageable, and you’ve initiated an emergency fund while also starting to invest.

This is a phase where confidence grows, signaling a shift from merely enduring to genuinely thriving. A critical action at this point is fortifying your emergency fund. A widely recommended guideline is to accumulate savings equivalent to three to six months of living expenses. This fund provides peace of mind, mitigating anxieties about unforeseen costs like appliance breakdowns or urgent dental care.

At this stage, you might also begin making more substantial contributions to your CPF account and regularly setting aside a portion (e.g., 10%) of your take-home pay for investments, often utilizing strategies like dollar-cost averaging.

4. Growth: Accelerating Your Assets

Upon reaching the “Growth” stage, your investments are demonstrating consistent appreciation, and you possess a clear awareness of your progress toward your financial aspirations.

This involves diligently tracking significant financial milestones, such as reaching your first S$100,000. Your diligent efforts are now yielding gradual and consistent advancement.

Consider strategies like incrementally increasing your investment contributions (e.g., by 1% annually). This phase also encourages deeper introspection into your financial purpose, prompting you to consider how your wealth can genuinely serve your values and desires.

5. Independence: Financial Freedom Achieved

“Financial Independence” signifies a pivotal point where your living expenses are fully covered by income generated from investments, real estate, or other passive sources, eliminating the need for traditional employment.

For some, this translates into early retirement. For others, it grants the freedom to engage in work purely out of passion, rather than necessity. Regardless of the form it takes, this stage represents the attainment of true financial liberation.

Achieving independence typically demands extensive long-term planning, unwavering discipline, resistance to “lifestyle creep,” and a high savings rate. The emotional rewards are profound, encompassing a sense of freedom, self-assurance, and autonomy.

This stage encourages a re-evaluation of personal definitions of wealth, whether it involves extensive travel or philanthropic endeavors. By clearly articulating what prosperity means to you, your financial goals and management become more intentional.

6. Abundance: Living Generously and Purposefully

Having attained “Abundance,” you now possess surplus wealth that enables generous living and investment in broader, more impactful goals.

This level allows for worry-free funding of children’s education, substantial charitable contributions, entrepreneurial pursuits, or engaging in creative endeavors without financial constraints. Your wealth now powerfully supports both your personal needs and your overarching purpose.

At this stage, your finances are typically managed with the professional guidance of financial planners or legal advisors. The focus shifts to refining these professional relationships and actively exploring opportunities for philanthropy, whether through monetary donations or sharing your expertise.

7. Legacy: Enduring Impact

The ultimate stage of wealth is “Legacy,” characterized by a long-term perspective that extends beyond your lifetime. Financial decisions at this level are meticulously crafted to create lasting impact for future generations.

This involves intricate estate planning, establishing charitable foundations, and orchestrating intergenerational wealth transfers. Your aim is for your wealth to benefit your family, community, and values long after you are gone.

Legacy building transcends mere financial inheritance; it also encompasses the values and principles you instill. This is where accumulated wealth gains profound meaning, leading to comprehensive estate planning, the formation of trusts, and strategic approaches to ensuring your financial legacy benefits those you care about for decades to come.

Strategies for Advancing Through the Wealth Stages

The progression through these wealth levels is rarely linear, mirroring the unpredictable nature of life and investment journeys. Unforeseen events—such as job losses, medical emergencies, or prolonged market downturns—can occur.

The most crucial element is to establish a robust framework that enables adaptation and continuous advancement up the wealth pyramid. Cultivating sound financial habits is paramount. This includes diligently tracking all expenditures to maintain a clear understanding of your income, expenses, assets, and liabilities. Beyond this, consistent and early saving is vital, as it allows for the powerful effect of compounding once investments begin.

It is essential to remember that wealth accumulation is a process that spans decades, devoid of any “get rich quick” shortcuts. By committing to ongoing learning and self-education—from budgeting effectively to making informed investment decisions—you can significantly enhance your journey toward financial well-being.

If you’re reading this, you must be trying to figure out the best course of action right now: is it the right time to buy or sell?

It’s difficult to give an exact answer since everyone’s situation is unique and what works for one person may not necessarily work for you.

I can bring you a wealth of on-the-ground experience and a data-driven approach to provide clarity and direction. From beginners to experienced investors, our top-down, objective approach will help you on your real estate journey.

I can help you by:

You May Also Like …

A password will be e-mailed to you